Understanding the Fast-Growing Drone Market

Drones (not the lazy bee variety), also referred to as unmanned aircraft system (UAS) or unmanned aerial vehicles (UAVs), represent one of the fastest growing global product markets. While drone usage in civil applications in increasing, military applications continue to dominate the UAV market. Ukraine has famously (and successfully) been innovating drones for naval warfare as well as land operations.

Drones have been employed across various sectors for many years because of their ability to perform tasks in challenging environments where human access is difficult. They are invaluable for operations requiring speed and precision, from combat missions to express shipping and delivery. They are also inexpensive, especially when compared to the substitutes but they also solve problems for which there are no substitute economic goods.

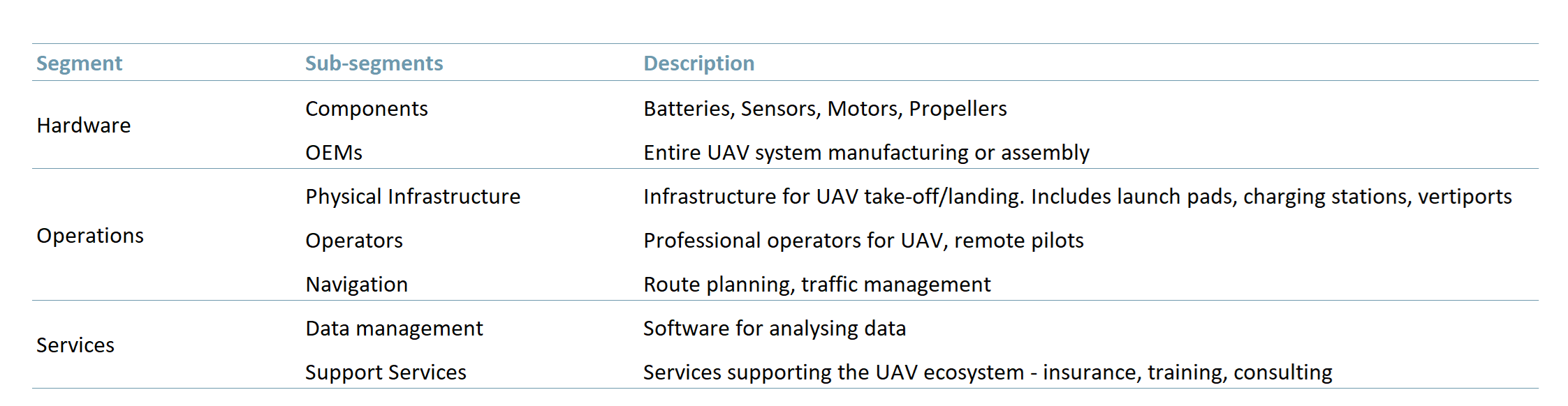

Understanding the drone value chain enables investors to identify key components and stakeholders, guides strategic investments, enhances efficiency and innovation for users and developers. The value chain can provide insights into supply chain management, regulatory compliance and market trends. It can enable improved decision-making, resource allocation and adaptation to market trends.

The drone market value chain comprises three core investment areas:

- Hardware: Includes components used in the manufacturing of drones such as motors, propulsion systems, payloads, communication modules, batteries, power systems and propellers.

- Operations: Involves the physical infrastructure for UAV take-off and landing and training and provision of professionals to operate UAVs and navigation systems for smooth functioning of UAVs in airspace.

- Services: Includes the software needed to analyse data collected by drones.

Exhibit 1 – Drone value chain

Sources: ACF Equity Research Graphics; McKinsey & Company.

Sources: ACF Equity Research Graphics; McKinsey & Company.

Military applications and the geopolitical context

Drones are revolutionising warfare by offering increased convenience and flexibility at lower costs while minimising human casualties (at least for those using the drones). Their success in military operations has driven demand in North America, the Middle East, and Asia-Pacific. Drones are becoming essential in military intelligence and surveillance, and are rapidly expanding into other combat areas (viz Ukraine’s naval efforts).

Recent geopolitical events such as the Russia-Ukraine war and Israel-Palestine conflicts, have demonstrated the deployment and effectiveness of advanced military drones. These drones facilitate targeted strikes for nations and decrease the risk to civilian lives and to the forces deploying the drones. This is not only related to their relative precision and speed but also in no small part to their ability to remain on standby and engage at optimal times.

Global defence spending demand driver

Rising geopolitical tensions have prompted countries to increase their defence budgets, which has likely boosted growth in military UAV systems. According to the US Presidential budget for fiscal 2024, the US Department of Defense plans to accelerate the deployment of advanced combat drones as part of a broader initiative to modernize its military by embracing cutting-edge technology.

The US Air Force is requesting $5.8 billion to develop 1,000 AI-driven unmanned combat aircraft under its next-generation air dominance program. These autonomous aircraft are ideal for executing high-risk missions and safeguarding pilots.

The United States is not alone in ramping up defence spending on unmanned aerial vehicles. Other countries such as Germany and Japan have approved a significant increases in spending on armed drones in recent years. Japan allocated 182.7bn yen (~US$1.2bn) on military drone purchases in 2023.

Israel has maintained a prominent position in global UAV technology, utilising drones for diverse military purposes for over a decade. Israel’s three major defence companies — Elbit Systems, Rafael Advanced Defense Systems and Israel Aerospace Industries (IAI) — are key players in the UAV market. Elbit produces the large Hermes 900 drone, while IAI offers the Heron line of drones. Rafael, as a part owner of Aeronautics, is involved in the production of the Orbiter series of drones.

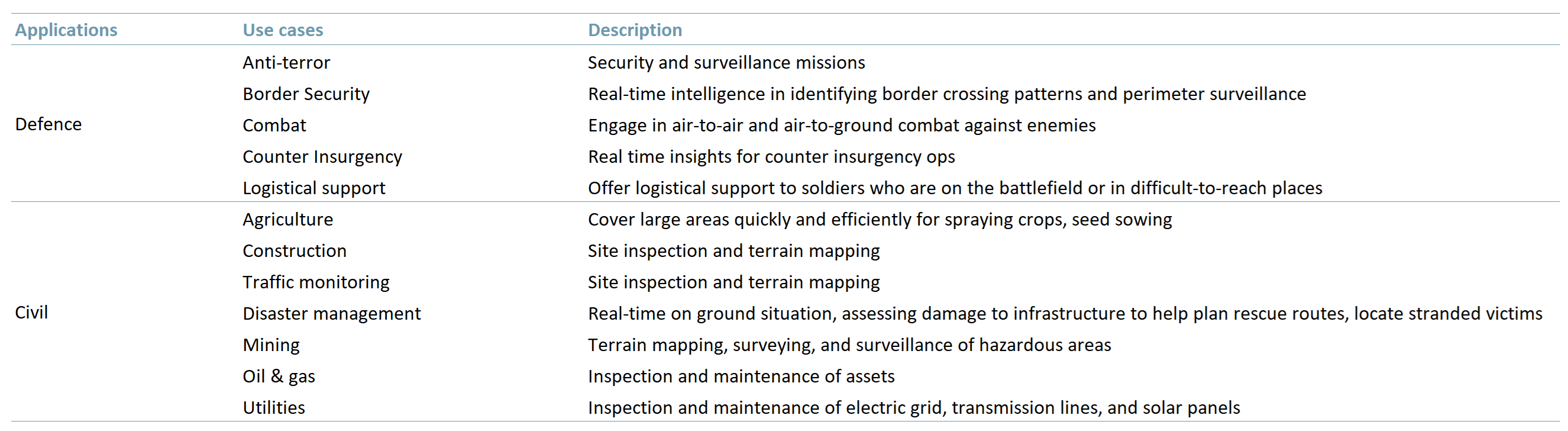

Civil and commercial applications – by far the largest opportunity

In addition to military capabilities, drones are increasingly used in civil and commercial applications, which lies in their ability to enhance efficiency, reduce costs and improve safety across industries. Drones can revolutionise agriculture through precision farming, expedite construction and infrastructure projects, and provide support in disaster response.

Drones are already used and have growing potential in detailed surveying and mapping by providing insightful analytical data for crowd and traffic management, e.g. crowd density, movement patterns, behavioural analysis, accident detection, route optimisation etc..

Because drones are not just a relatively inexpensive substitute but also solve old problems in new ways. Integrating drones in industrial processes and applications is driving regulatory change and is a source of technological advancement, which in turn fosters its own innovations and so economic growth. Drones are transformation. Investors tend to obtain returns outperformance from transformations.

Exhibit 2 – Drone use cases

Sources: ACF Equity Research Graphics; ideaForge.

Sources: ACF Equity Research Graphics; ideaForge.

Safety, privacy and regulatory barriers remain key challenges for the rapid adoption of UAVs. The most urgent challenge for governments is to ensure that the drone operations remain safe and secure. Fortunately, the regulatory landscape appears to be moving in the right direction, enabling the creation of a more conducive environment for drone integration.

Through innovative approaches and favourable policy making, drones are positioned to deliver significant economic and societal benefits – enhanced safety, speed, cost-effectiveness and efficiency.

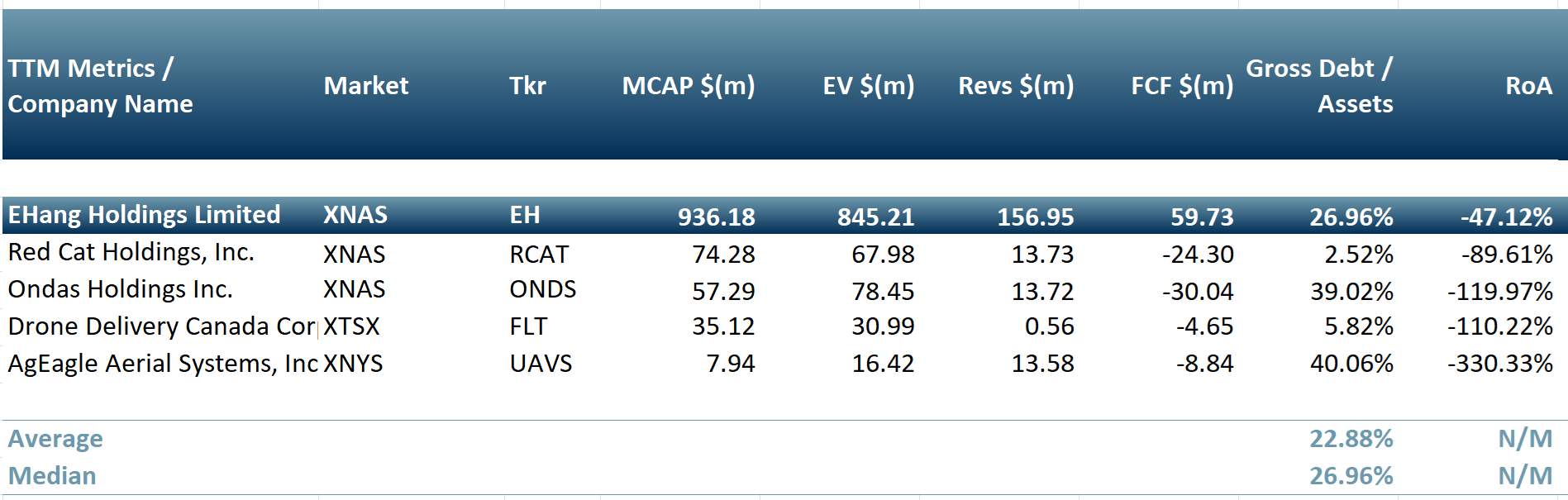

In exhibit 3 below, we highlight a small group of emerging, publicly listed, companies involved in the drone value chain.

- EHang Holdings Limited (Nasdaq : EH) – Develops autonomous aerial vehicles (AAVs) for passenger transportation and logistics.

- Red Cat Holdings, Inc. (Nasdaq : RCAT) – Provides products, software services and solutions to the drone industry.

- Ondas Holdings Inc. (Nasdaq : ONDS) – Provides private wireless data and drone solutions for mission-critical services and industrial markets.

- Drone Delivery Canada Corp. (TSXV : FLT.V) – Focuses on design, development and implementation of its proprietary software platform using drones.

- AgEagle Aerial Systems, Inc. (NYSE : UAVS) – Provides drone solutions for precision agriculture and industrial uses.

Exhibit 3 – Peer group of companies involved in drone manufacturing

Sources: ACF Equity Research Graphics; Refinitiv.

Sources: ACF Equity Research Graphics; Refinitiv.

{kind=link}