New Horizons – UK Healthcare Devices Market

Medical devices (which includes software) approval is to be speeded up, to help develop the UK SME medical devices sector opportunity, through an approach that also raises risk classifications, which could seem contradictory.

The Medicines and Healthcare products Regulatory Agency (MHRA) will introduce changes to the UK medical devices regulatory framework by 2025 to prioritise patient safety. These changes aim to improve key aspects of the industry, which generates an annual turnover of ~US$34bn, YE22A. This blog attempts to deliver a distilled analysis of the market drivers, key segments, challenges and opportunities that are shaping the landscape of medical technology in the UK.

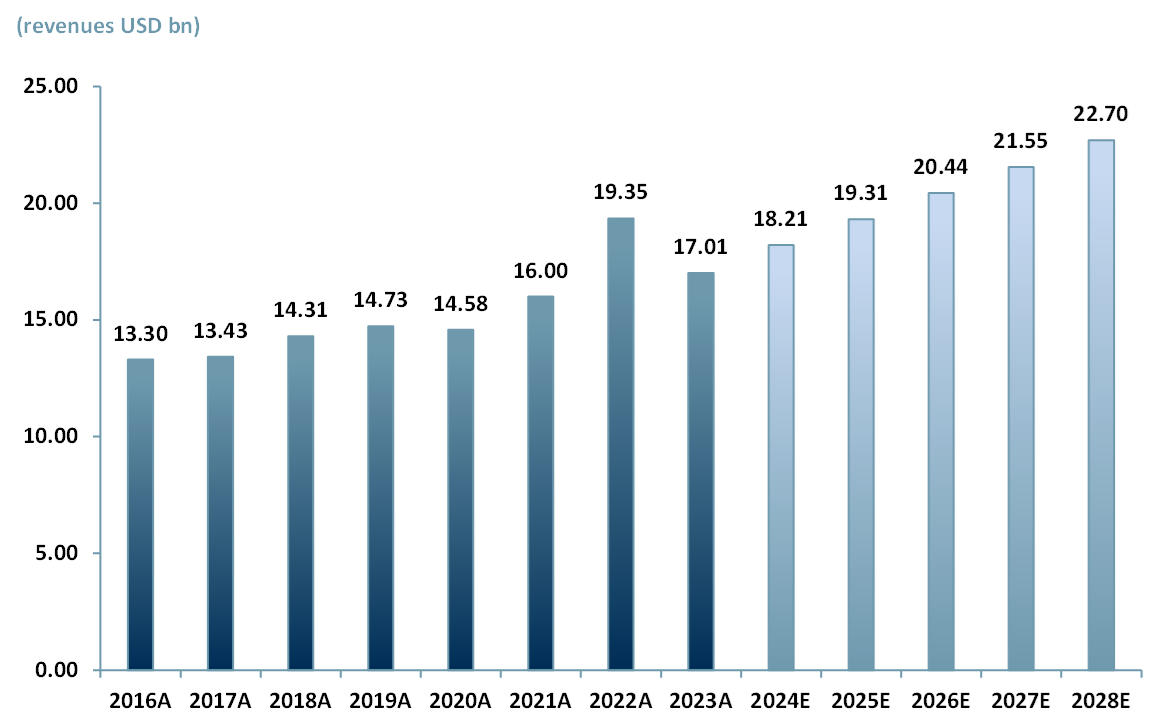

By 2028E, the UK medical devices market is forecasted to reach US$22.68bn up from a forecasted US$18.21bn, by the end of this year (2024)E, representing a CAGR of 5.64%. Cardiology devices is the largest market sub-segment, forecasted to reach US$2.67bn by 2024E. In comparison, the UK market opportunity whilst valuable is approximately 10% of the value of the US medical devices market, forecasted to reach US$182bn in 2024E.

The UK medical devices market saw a spike in 2022 (exhibit 1) following the Covid-19 pandemic. This was in part driven by the excess of 29% in the healthcare budget provided by the government in 2021. The pandemic further accelerated the need for digital health technologies, including telemedicine and wearable devices.

Exhibit 1 – UK medical devices market (revenues) 2016A-2028E

Sources: ACF Equity Research Graphics; Statista.

Sources: ACF Equity Research Graphics; Statista.

In January 2024, the UK’s MHRA, an executive agency of the UK’s Department of Health, published a roadmap for the new regulatory framework signalling enhancements to the governance of 3.25m+ registered medical devices. The UK’s National Health Service (NHS), which delivers ~86% of the UK’s healthcare services, introduced in Feb, 2024 a strategy to integrate and maximize the value of Small and Medium Enterprises (SMEs) involved in the patient care market (GOV.UK, 2024).

These UK government initiatives are aimed at improving patient safety and advancing medical technology. The UK initiatives will include, but are not limited to, implantable devices, AI, diagnostics for early detection and prevention. What is driving this change?

Growth Drivers

- Aging Population: The number of UK residents over 85 is forecasted to reach 2.6m by mid-2026E up from 1.6m in 2021A. The growing elderly population will or does require advanced chronic disease management and innovative healthcare solutions (Office of National Statistics, 2024).

- Technological Innovations: Technological innovations, such as high-definition laparoscopic instruments could boost exports. In March 2022, Surgical Innovations (LSE:SUN) launched YelloPort Elite™ – an innovative hybrid technology that aims to cut the carbon footprint and plastic waste produced by the Port Access Systems.

- Government Initiatives: Supportive UK government policies promote medical devices innovation. For example, the Innovative Devices Access Pathway (IDAP) pilot, launched in Sept. 2023. This pilot pioneers the testing of components in the end-to-end innovation pathways for medical devices intended to be marketed in the UK. Amongst the already chosen eight technologies within the IDAP pilot is a blood test diagnosis pilot for the neurodegenerative disease (NDD) Alzheimer’s and an AI for assessing chronic obstructive pulmonary disease risk (GOV.UK, 2024).

Key Segments

- Diagnostic Devices (MRI, CT, blood tests): Diseases like diabetes and cancer are on the rise (environmental, lifestyle, nutrition and demographic drivers). Early detection does much to enhance positive clinical outcomes. These factors are fuelling demand for real-time diagnostic devices. Between Feb. 2022 and Jan. 2023, 43.4m imaging tests were conducted in England. There are currently 155 operational community diagnostic centres (CDCs) that use devices such as MRI, CT, X-ray to improve early diagnosis of life-threatening diseases. By 2025 the NHS plans to open 160 CDCs (GOV.UK, 2024).

- Therapeutic Appliances: This medical devices market sub-segment includes essential patient survival devices such as respiratory machines, dialysis machines and insulin pumps.

- Wearable Medical Devices: The wearable devices market reached $1.2bn in 2023A, driven by increasing consumer health awareness and a demand for portable healthcare devices, e.g. smartwatches, implantable devices, insulin monitors, wearable pain reliever devices and respiratory therapy devices (Grand View Research, 2024).

The growth horizon for the UK healthcare devices market is promising, but like any industry there are challenges, which can of course lead to opportunities. It is worth recalling that most new successful growth businesses that are currently household names were started during a period of negative change in the economic climate of the general economy or a sub-sector of the economy, i.e. under economic pressure.

Challenges

- Regulatory Landscape: Stringent regulations and Brexit have impacted supply chain operations and classification standards. The MHRA is considering a material review of medical devices under the Classification of General Medical Devices, which are currently graded into four classes based on level of risk (Class I = low risk, Class IIa = medium risk, Class IIb medium risk, Class III = high risk). The implication is that for example, in vitro fertilisation (IVF) and assisted reproduction technologies (ART) could be reclassified upwards for risk as Class III vs. Classes I & II (GOV.UK). The MHRA is also apparently intending to release SaMD guidance on Good Machine Learning Practice and AI as a Medical Device (AIaMD). This aims to clarify regulatory requirements for software and AI, ensuring patient protection. On 9 May 2024, MHRA launched the AI-Airlock – new regulatory sandbox for AIaMD – a project designed to test a range of regulatory issues for these devices in order to speed up AI medical device development and deployment (Compliance & Risks, 2024).

- Cost Constraints: High costs associated with advanced medical devices can hinder market growth, particularly in cost-sensitive settings by requiring constant funding. For e.g. in October 2023, the £30m Health Technology Adoption and Acceleration Fund (HTAAF) was established to help integrated care systems (ICSs) invest in medtech to manage winter healthcare demand pressures.

- High Competition: The UK healthcare devices market demands innovation and partnerships. The NHS is the largest buyer, sourcing over 80% of devices from imports, with the US as a leading supplier (International Trade Administration, 2023). There is a two way opportunity here to be exploited.

Opportunities

- Digital Health Solutions: The integration of AI and IoT in medical devices is growing. Digital innovation is vital to the 10 year plan or NHS Long Term Plan, which includes ‘digitally enabled care’ by 2024 – the right to access digital primary care services (online consultations), to have care at home supported by remote monitoring (wearable devices) and digital tools is becoming enshrined, at least in the minds and demands of patients. In our assessment, digital technology will accelerate the drive for service transformation, including outpatient service redesign and the reorganization of pathology and diagnostic imaging services (International Trade Administration, 2023; Kings Funds, 2019).

- Training and Education: Increased investment in training healthcare professionals on the latest digital technology and, for example, laparoscopic techniques can lead to an expanded market base and enhance service quality.

- Export Potential: The UK is recognised globally for manufacturing quality, innovation and compliance. The UK exported $5.4bn worth of medical technology in 2022A, underscoring its strong position in the global market (Office of Science, 2022).

The UK healthcare devices market is adapting and we propose, able to thrive, amidst advancing and evolving technological and regulatory landscapes – this presents a dynamic, opportunity filled, landscape for investors. With government initiatives fostering innovation and a clear trajectory towards integrating advanced medical technologies, the sector has the potential for substantial growth. Investors should closely monitor emerging trends, such as the rise of AI in medical diagnostics and the expansion of telemedicine, which are likely to redefine patient care and potential returns and so offer attractive high growth, capital transforming, investment opportunities.

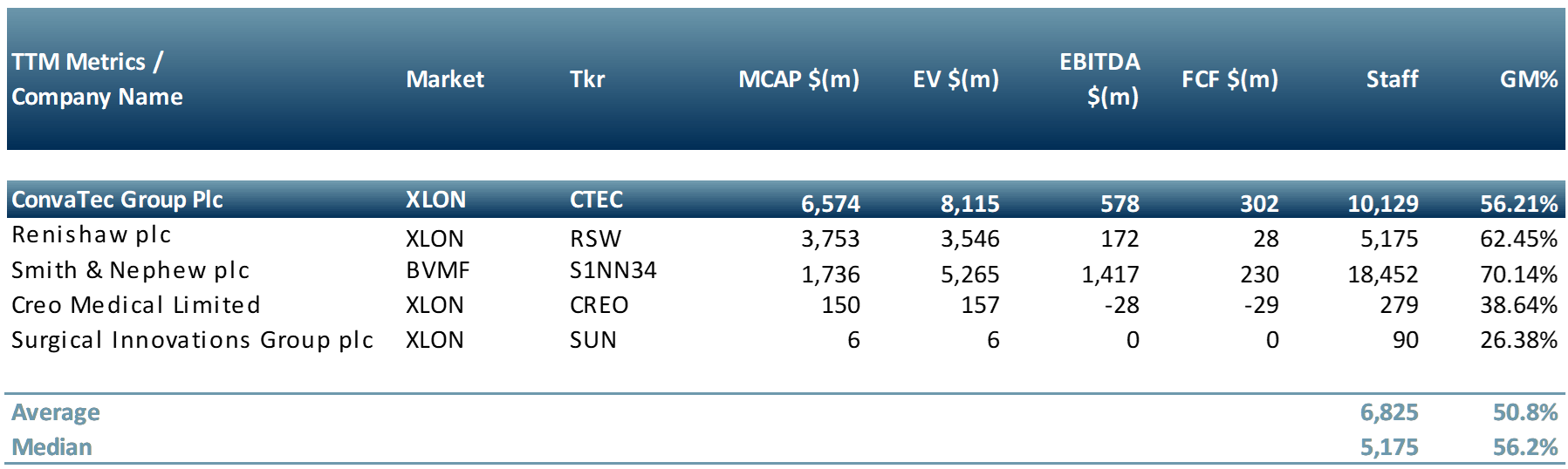

In exhibit 2 we highlight companies that are listed in the UK and are involved in the development, manufacturing and sale of medical devices. They include:

ConvaTec Group Plc (LSE:CTEC) – focuses on producing technologies for therapies in management of chronic conditions, including advanced wound care, ostomy care, continence care, and infusion devices. Headquartered in the UK, ConvaTec serves healthcare providers and patients in more than 100 countries.

Renishaw plc (LSE:RSW) – technology company with expertise in precision measurement and healthcare. Founded in 1973, Renishaw offers products and services in metrology, spectroscopy, and medical devices, including dental CAD/CAM, neurosurgery, and stereotactic radiosurgery.

Smith & Nephew plc (LSE:SN) – specializes in advanced wound management, orthopaedic reconstruction, sports medicine, and ENT (ear, nose, and throat) treatments. Founded in 1856, it operates in over 100 countries, providing innovative solutions to improve patient outcomes and enhance healthcare delivery.

Creo Medical Limited (LSE:CREO) – medical device company specializing in the development and commercialization of minimally invasive surgical devices, particularly for advanced energy-based surgery. Their flagship product, CROMA, is a cutting-edge electrosurgical platform designed to improve surgical precision and patient outcomes in gastrointestinal endoscopy and other procedures.

Surgical Innovations Group plc (LSE:SUN) – designs, develops, and manufactures innovative medical devices for minimally invasive surgery (MIS). Headquartered in the UK, the company focuses on providing high-quality, cost-effective solutions for laparoscopic surgery, enhancing patient recovery and reducing healthcare costs.

Exhibit 2 – Peer group of companies listed in the UK involved in medical devices

Sources: ACF Equity Research Graphics; Statista, Refinitiv.

Sources: ACF Equity Research Graphics; Statista, Refinitiv.

{kind=link}