Will cooperation between Healthcare firms continue as a trend, increasing healthcare M&A?

Siemens Healthineers (SHL.DE) announced that it would acquire Varian Medical Systems (VAR) on the 2nd of August 2020 for USD 16.4bn. Siemens will purchase all of Varian’s shares for $177.50/share in cash; a 24% premium.

The deal will be financed through debt and equity funding and is expected to close by 1H21.

This acquisition speaks to the growing trend of big pharma companies making a play for greater shares of the oncology market, which is expected to be worth $202.5bn by 2023, up from $77bn in 2017, a 163% increase. (Reportlinker, 2020)

Data from EvaluatePharma showed that over the last five years, about 41% ($120bn) of the total amount spent on deal-making activities was funnelled into the oncology market – a trend that we are likely to see continue through to 2022.

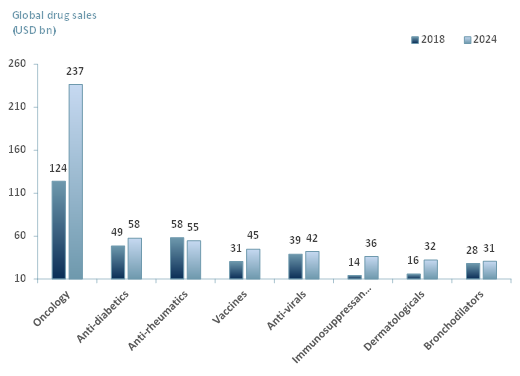

Oncology drug sales compared to other therapy areas are projected to reach $237bn in sales by 2024, up from $124bn in 2018 (a 91% increase). In Exhibit 1 below we see the global sales of prescription, including oncology and over-the-counter drugs by type in 2018 vs. 2024 forecast.

Exhibit 1: Global sales of prescription and over-the-counter drugs, 2018 & 2024

Sources: ACF Equity Research; EvaluatePharma

By 2024 the oncology drug market alone is expected to make up 80% of the total value of the other seven drug types, $236.6 vs. $298.1The growth in the market is driven by:

- The increase in the aging population – according to the United Nations World Population Prospects, the global population is expected to reached 9.3bn by 2050 and approximately 21% of it will be aged 60+.

- Improved purchasing power for the poor and middle class – globally families now have better access to quality healthcare as their standards of living rise.

- The substantial price tag on cancer drugs – the cost of one round of cancer treatment (chemotherapy, radiation therapy, immunotherapy, bone marrow transplant, hormone therapy, targeted drug therapy) is approximately $100,000 per patient. (Statista, 2020)

- Innovations in the healthcare industry and in particular oncology – advancements in biologics, cell therapies, bioelectronics, nucleic acid therapies and implantables.

All of the drivers above make the oncology market highly attractive to investors. Healthcare and technology inevitably go hand in hand.

In addition, as a result of Covid, we have seen healthcare facilities being forced to work together to support the demand strain on the sector. When companies work together, they begin to understand one another, and merging company cultures is a key factor in successful M&A.

We expect this cooperative bilateral approach between firms to continue as a trend, which in-turn will result in an increase in healthcare M&A. We expect M&A to continue unabated or to accelerate in 2021.

Another M&A drive in Pharma is the emerging market in biologics and biosimilars. While drug pricing and competition from biosimilars continues to add strain to pharma margins, pharmaceutical companies are looking to propel sales by both organically growing and boosting their cancer treatment portfolios via M&A.

As a result, we are likely to see robust deal-making activities in the coming years between big pharma and biotech oncology firms – akin to Pfizer’s (PFE) $10.64bn acquisition of Array BioPharma Inc. (ARRY) in 2019 for a premium of 62%.

{kind=link}