The weaponisation of semiconductors

Is the market for semiconductors a case study for Mark Galeiotti and weaponisation? In Mark Galeotti’s The Weaponisation of Everything, he presents the historical case for states using non-military strategies in their fight for victory.

The world is increasingly interconnected and ‘co-dependant’ and so the use of non-military means for waging ‘war’ is becoming more prominent.

‘Weaponisation’ is particularly evident in the commodities market. As a result of sanctions on Russia, Russia has placed a temporary ban on grain exports to ex-Soviet countries. (This is in addition to Moscow’s Black Sea blockade delaying exports from Ukraine to countries such as Yemen and Ethiopia).

The United Nations warns that Russia’s actions could trigger a global famine. Michael Fakhri, the UN’s special rapporteur on the ‘right to food’, says that “food should never be weaponised and no country in the world should be driven into famine and desperations.”

Weaponising semiconductors

Geopolitical tensions are impacting the semiconductor industry and exacerbating the Covid-19 triggered supply chain driven microchip shortage.

- Subjecting Russia to sanctions is exacerbating the global microchip shortage whilst the US and EU spend billions in a race against China for total microchip production dominance;

- IntelCorp (Nasdaq: INTC) – supplier of microprocessors to Acer (TPE:2353), Lenovo (HKG:0992), HP (NYSE:HP), Dell (NYSE:DELL) – plans to build a €17bn(~$18.7bn) factory in Magdeburg (East Germany) with production expected in 2027E;

- This is part of CEO Pat Gelsinger’s plan to de-risk Asian (i.e. Chinese) production chains and tackle the global chip shortage as a result of Covid and the current geopolitical tensions. The EU-US joint venture, backed by US$100bn, aims to decrease EU and US reliance on Chinese imports and turn Germany into a chip powerhouse;

- Is it too little too late? Market sentiment suggests that this EU-US microchip JV in Germany might be a little too late and that there will, inevitably, be political strings attached to the funds for the project, complicating things further;

- CEO Rudi De Winter of XFAB Silicon Foundries SE (a chipmaker) says it is best not to disrupt the current supply chain as it is global, and fully integrated. The US-EU microchip production plan looks political rather than industrial in Mr De Winter’s view.

China’s dominance

Semiconductor supply is a political tool. The supply of semiconductors to Russia was one of the first goods that Brussels and Washington, DC. attempted to ban. This was followed by a ban on the purchase of Russian oil and gas and more recently, the US has restricted exports of luxury goods to and from Russia.

These bans are not specific to Russia however. The US’ Secretary of Commerce Gina Raimondo set out clearly that if China is to defy US exporting restrictions against Russia, the US will cause Chinese companies to shut down by cutting those companies off from the US manufacturing equipment and software China needs for its chip production industry.

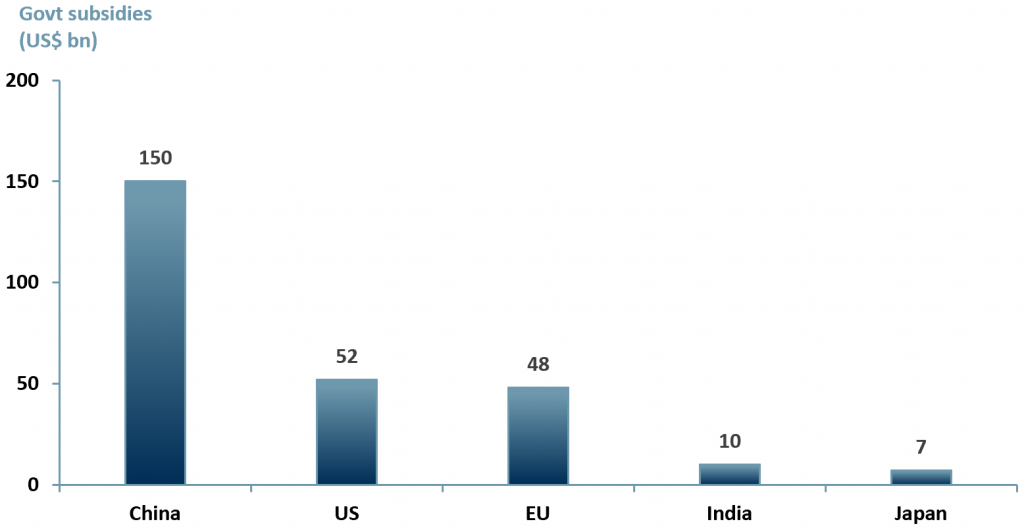

But what does this mean for the semi-conductor industry? China’s government currently ranks #1 globally for semiconductor industry subsidies, with offers totalling ~$US$ 150bn versus the US and EU combined subsidy offering of $100bn (exhibit 1)

Exhibit 1 – Semiconductor government subsidies by region (to date)

Sources: ACF Equity Research Graphics; Semiconductor Industry Association

Sources: ACF Equity Research Graphics; Semiconductor Industry Association

Others are following the Chinese and US-EU leads. The Japanese government has promised significant aid to the semi-conductor industry to encourage a $7bn factory planned by TSMC (TPE:233) and in partnership with SONY (NYSE:SONY) and DENSO Corporation (OTCPNK:DNZOY). The South Korean government has already started investing in its domestic chip market and has a plan for investments of up to $450bn by 2030E.

While this does not mean the US and EU are out of the running, it does mean that in the short to medium term their dependence on Asa will continue. The EU currently has a 9% share of the global semiconductor market and is aiming to raise that share to 20% by 2030E.

Is there a small to mid-cap opportunity in semiconductors?

The current geopolitical tensions do not necessarily mean that Asia will continue to dominate the market long term, though it is clearly responding to EU-US initiatives. In the US many smaller companies, listed on the NASDAQ, are catching the interest of investors.

Government support and increased funding will provide opportunities for these smaller players to establish valuable footholds in the semiconductor market. It is here and now that we see an opportunity for smaller US and EU companies to benefit from the strategic plan to compete with Asia and de-risk supply chains.

The Russia-Ukraine war only serves to increase US-EU political focus and accelerate a semiconductor supply chain de-risking strategy.

Nevertheless, the markets are on edge. Russia’s invasion of Ukraine has not been the short sharp shock generally feared and anticipated by the international community. Moreover, signs of a future diplomatic resolution are sparse.

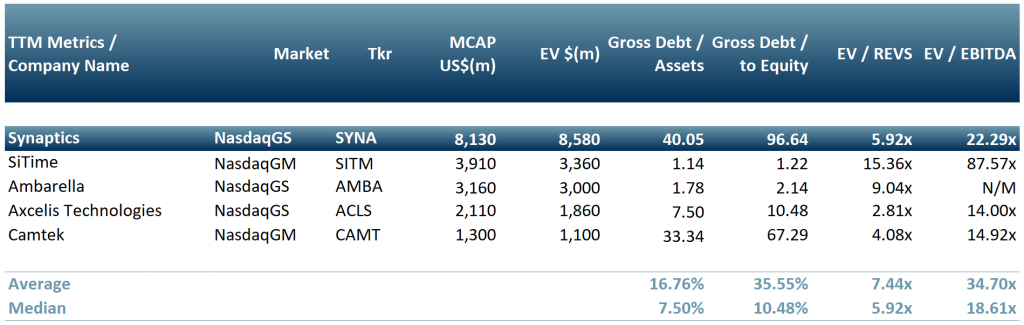

In exhibit 2 we present a peer group of the top five publicly traded small-cap companies in the semi-conductor space:

Synaptics (NasdaqGS:SYNA); SiTime (NasdaqGM:SITM); Ambarella (NasdaqGS:AMBA); Axcelis Tecnologies (NasdaqGS:ACLS); Camtek (NasdaqGM:CAMT). Our peer group could provide renewed high growth opportunities for investors with a penchant for semiconductor exposure.

Exhibit 2 – Peer group of US listed smaller and mid-cap semiconductor companies

Sources: ACF Equity Research Graphics; Refinitiv

Sources: ACF Equity Research Graphics; Refinitiv

Author: Renas Sidahmed – Renas is a Staff Analyst and part of the Sales & Strategy team at ACF Equity Research. See Renas’s profile here

{kind=link}