Chip makers move out of China

Intel, US chip maker wants to spread its $20bn investment plan out to 2030 across the EU.

Intel’s (Nasdaq: $INTC) plan is to establish two factories in EU with 10-yr operational lifespans. It is possible that total investments in the plants could rise to US $100bn, up from the initial $20bn commitment.

- Intel already has a factory in Ireland and plans to double its capacity through a US $7bn investment. The US chipmaker is yet to decide the new sites for the proposed European sites.

- Intel also plans to catch up with its Asian competitors Taiwan Semiconductor Manufacturing Company (NYSE: $TSM) and Samsung Electronics Co(KSE: $005930.KS) by starting the production of 7nm chips at the Irish plant and eventually 2nm chips in the proposed new EU factories.

There is a global semiconductor shortage – chip manufacturing companies such as Intel, TSMC and Samsung are planning more capacity to close the gap. The semiconductor companies have a challenge, which is to be able to source enough raw material to act as feed stock for the new planned capacity.

There is also concern over Intel’s EU proposition over the fate of the factories once their 10-yr lifespan is exhausted. If the retirement of the factories is not in the plan at the start, there are potential environmental and social issues at end-of-life.

Semiconductor manufacturers need to be as ESG compliant as any company on the global markets, if they wish to continue to attract investment capital. In our view, semiconductor manufacturing plants could be repurposed for different uses at end-of-life, including chip assembly or electronic components for EV cars.

Nevertheless, the increased interest from semiconductor producers to expand their production across the globe seems more of a strategic de-risking move out of China. The C-19 pandemic taught the world a valuable lesson about logistics (supply risk) – the manufacturing of any product should not be concentrated in only one country – e.g. China, regardless of local cost advantages.

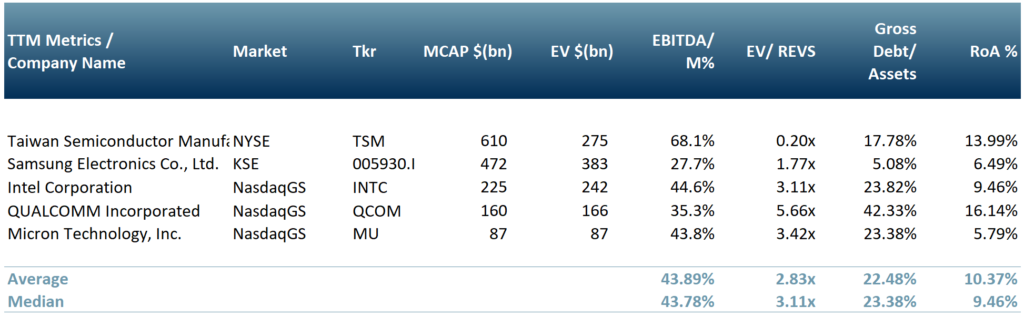

Below in exhibit 1 is our peer group table, which includes some of the top chip manufacturers by market cap:

Exhibit 1 – Peer group table few of the top semiconductor manufacturers on 15 July 2021

Source: ACF Equity Research Graphics; Notes: Exchange Rate (Source: XE.com) Currency Translation: KRW vs. USD 0.0009

Source: ACF Equity Research Graphics; Notes: Exchange Rate (Source: XE.com) Currency Translation: KRW vs. USD 0.0009

The sectors that generated the highest demand for semiconductors in 2019 were Communications (33%), PC/Computer (28.5%) and Consumer (13.3%) followed by Automotive (12.2%) and Industrial (11.9%). While in 2020 the sales of logic chips rose by 11.1%, followed by sensors at 10.7% and memory at 10.4%.

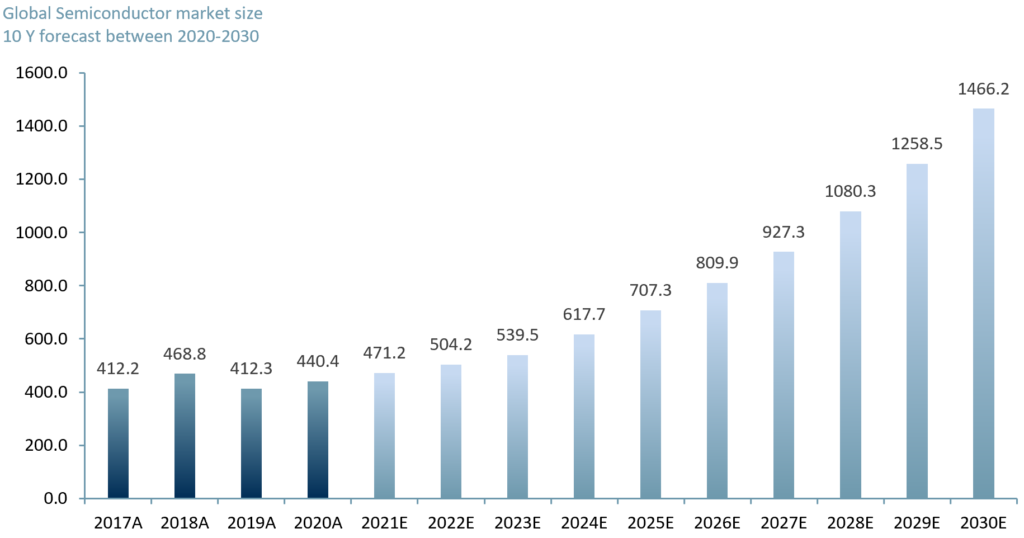

According to the Semiconductor Industry Association (SIA) the global semiconductor industry market size in 2020 was valued at US$ 440bn, 6.8% up from 2019. In April 2021, the SIA announced that 1Q21 chips sales increased by 17.8% vs. 1Q20.

Based on this data, World Semiconductor Trade Statistics forecasted a 19.7% surge in semiconductor sales, reaching US $527bn in 2021. ACF Equity Research projects a slower rise in sales for 2021, at 7% growth, due to the current lag in the supply chain that is likely to carry on until 2022. We also assess that this lag with slow growth will slow market growth until 2023.

Over the same period we expect that the dominant semiconductor manufacturers will have invested in expanding production capacity by building additional factories across the globe. Moreover, the manufacturing of advanced semiconductors of 7nm and 2nm will have increased worldwide.

In our forecasts, a chip sales rally will emerge from 2024E onwards at a CAGR of 12.78%. By 2030E we project that the semiconductor market size will reach US$ 1466bn, as per exhibit 2 below.

Exhibit 2 – Semiconductor market size worldwide plus ACF 10-yr forecast 2021E – 2030E

Sources: ACF Equity Research Estimates, World Semiconductor Trade Statistics

Sources: ACF Equity Research Estimates, World Semiconductor Trade Statistics

The closer it gets to the 2035 deadline for the cessation of sales of petrol/diesel cars, the higher the demand for EV and green energy (probably hydrogen) vehicles. We see the ‘rush’ to transition to EV and green as a major demand driver for semiconductors.

We have entered into an era of transformation, where within 1-2 decades, any means of transport will be electric/green energy and more or less fully automated. Besides regular EV cars/vans manufacturing, the production of flying taxis and delivery drones are possible developments that will add to semiconductor demand.

The communication and industrial sectors will increase their demand for semiconductors. Working from home will likely be a combinatorial new normal for most businesses and mobile/online communication might replace a lot more face-to-face socialisation, than is currently expected.

Within the industrial sector, healthcare is bound to require an enhanced number of semiconductors as the sector is already incorporating AI solutions and IoT in most medical devices, and possibly even in people to enable home health monitoring and personalised medical care that is also affordable for insurers and or the state.

For the surge of chip manufacturing to be sustainable and for prices of raw materials to avoid becoming a restriction to growth of the chip sector, we expect a renewed focus on recycling processes and technology as part of our sector read through for investors. Our 10 year view, with notable individual stock exceptions, the sector looks broadly under rated even at today’s expanded valuation multiples (expanded multiples are observable across most if not all global equity classes).

Author: Anda Onu – Anda is part of ACF’s Sales & Strategy team. See Anda’s profile here

{kind=link}